For many businesses, one of the first questions when exploring the R&D Tax Incentive (RDTI) is straightforward one:

How much financial support can we actually receive?

Unlike traditional grants, the RDTI does not provide a fixed funding amount. Instead, it operates through a tax offset mechanism, offering a percentage-based benefit on eligible R&D expenditure already incurred.

Once R&D activities are completed, registered, and successfully claimed through the tax system, businesses may benefit in the following ways:

· Offsetting current income tax liabilities

· Receiving a cash refund (subject to eligibility)

Understanding how this mechanism works allows businesses to more accurately assess the true cost of R&D and incorporate the incentive into both strategic decision-making and financial planning.

1. Core Calculation Logic of the R&D Tax Offset

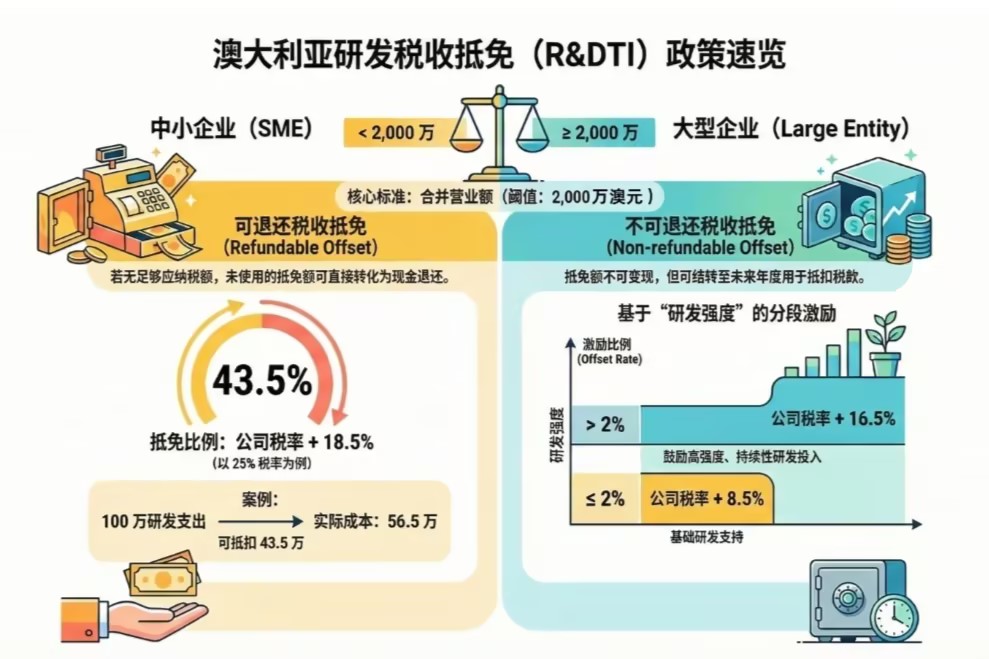

Under the RDTI framework, the level and type of support primarily depend on a company’s size, determined by aggregated turnover

This is not limited to the revenue of a single entity. It includes the broader economic group, such as:

· Connected entities

· Affiliates

For companies with group structures or ownership links, eligibility thresholds must be assessed on a consolidated basis.

1.1 Small to Medium Enterprises (< AUD 20 million)

Where aggregated turnover is below AUD 20 million, companies are generally eligible for a refundable R&D tax offset

The offset is calculated as follows:

Corporate tax rate + 18.5%

For example:

· At a 25% tax rate → 43.5% offset

· At a 30% tax rate → 48.5% offset

It is important to note that this is not a direct grant. It remains a tax offset.

However, where the company does not have sufficient taxable income, the unused portion may be refunded as cash, subject to eligibility criteria.

Note: In certain cases (e.g. where the company is controlled by exempt entities), the offset may not be refundable.

1.2 Large Enterprises (≥ AUD 20 million)

Where aggregated turnover reaches or exceeds AUD 20 million, companies are generally eligible for a non-refundable R&D tax offset.

Key characteristics:

· Cannot be converted into cash

· Can only be used to offset future tax liabilities (carry-forward rules apply)

For larger entities, the incentive rate is linked to R&D Intensity

R&D intensity is typically defined as:

R&D expenditure ÷ Total Expenses

This metric reflects how much of a company’s overall spending is directed toward R&D.

For large companies, the RDTI applies a tiered (incremental) structure:

· Up to 2% intensity:

Corporate tax rate + 8.5%

· Above 2% intensity:

Corporate tax rate + 16.5%

The key point:

Only the portion above the 2% threshold receives the higher rate — not the entire R&D spend.

This structure is designed to incentivise increased and sustained R&D investment, rather than minimal compliance at threshold levels.

2. Illustrative Examples

Example 1: SME Scenario

Assume a technology company with:

· Aggregated turnover: AUD 8 million

· R&D expenditure: AUD 1 million

· Corporate tax rate: 25%

· Eligible for refundable offset

Calculation:

1,000,000 × 43.5% = AUD 435,000

Subject to eligibility, this amount may be used to offset tax or received as a refundable tax offset.

Effective R&D cost (illustrative): AUD 565,000

This is why many businesses view the RDTI as a form of non-dilutive funding.

Example 2: Large Company (Tiered Calculation)

Assume:

· Aggregated turnover: AUD 50 million

· Total expenditure: AUD 20 million

· R&D expenditure: AUD 1 million

· R&D intensity: 5%

Breakdown:

· First 2% (AUD 400,000):

→ Tax rate + 8.5%

· Remaining 3% (AUD 600,000):

→ Tax rate + 16.5%

The offset must be calculated incrementally, rather than applying a single blended rate.

3. Cap on Eligible R&D Expenditure

For income years starting on or after 1 July 2021, a key threshold applies:

Concessional Cap: AUD 150 million per annum

Expenditure within the cap is eligible for full RDTI rates.

Expenditure above the cap is only deductible at the standard corporate tax rate (with no additional uplift).

This ensures the incentive is distributed across a broader range of businesses, rather than concentrated in a small number of very large projects.

4. Eligibility Requirements

The RDTI does not automatically apply to all R&D expenditure. Key conditions typically include:

· The claimant must be an eligible R&D entity (generally an Australian company)

· Activities must qualify as eligible R&D activities (core or supporting)

· Expenditure must qualify as eligible R&D expenditure

· A minimum R&D expenditure threshold of AUD 20,000 in notional deductionsgenerally applies (unless conducted through a registered Research Service Provider)

Ultimately, eligibility depends not just on how much is spent, but whether the activities are technically eligible and compliance-ready.

5. What Does the RDTI Mean for Businesses?

From a financial management perspective, the RDTI can have a meaningful impact on a company’s funding structure:

Cost recovery

A portion of R&D expenditure can be effectively recovered through the tax system, reducing overall project cost.

Cash flow improvement

For SMEs in particular, refundable offsets can generate significant cash inflows to support ongoing development.

Improved return on innovation

Factoring in the RDTI can materially change the ROI profile of R&D investments, making sustained innovation more viable.

Conclusion

The true value of the RDTI lies not in a one-off tax benefit, but in its ability to reshape the cost structure of innovation.

By reducing financial uncertainty, it enables businesses to:

· Plan R&D investment with greater confidence

· Sustain long-term innovation strategies

· Align technical development with financial efficiency

For companies actively engaged in technology development, understanding how the RDTI is calculated is not just a compliance exercise—it is a strategic lever for building durable competitive advantage.